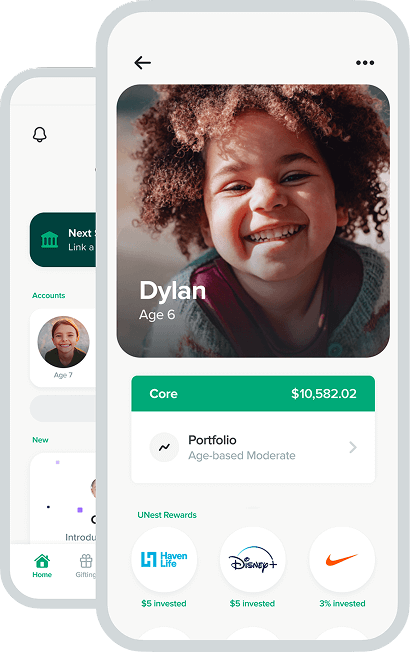

Family investing made easy

Build a brighter future for your kids. Join the growing community of parents that save and invest with UNest.

Get StartedAS SEEN IN

UNest is the market leader in tax-advantaged custodial investment accounts* for kids.

* Investment advisory services offered through UNest Advisers, LLC, an SEC-registered investment adviser.

One Year Free

No fees on balances up to $300 for the first 12 months

What’s better than watching your kid’s money grow?Watching it grow for free.

after your first year or $300+ balance

$2/mo + 0.25% annual

no surprises

Rewards

Hundreds of brands are waiting to invest in your kid’s future for making purchases you would make anyway.

Gifting

Invite your friends and family to invest alongside you in your kid’s financial future.

Protection

Give your family more than just a head start — give them financial security.

Term life insurance through

4.7 star app store rating

UNest Savings Calculator

Adjust the numbers to explore how your savings could add up.

Get the App

All investing involves risk.

This website is operated by UNest Holdings, Inc. Investment advisory services are offered through UNest Advisers, LLC, an SEC-registered investment adviser. Brokerage services are provided to clients of UNest Advisers by UNest Securities, LLC, an SEC-registered broker-dealer and member of FINRA and SIPC.

Client accounts are protected by the Securities Investor Protection Corporation (SIPC) for up to $500,000, which includes a $250,000 limit for cash. SIPC protection does not cover market losses. For details, please visit www.sipc.org.

UNest does not provide investment advice on bank products or any investments that are guaranteed or insured by the FDIC or any other government agency. Investing involves risk, and investments may lose value. Please consider your investment objectives, risk tolerance, and UNest pricing before investing. Past performance does not guarantee or indicate future results.

Any investment projections, performance charts, or illustrative outcomes shown are hypothetical, for informational purposes only, and do not reflect actual investment results. They are not guarantees of future performance.

UNest does not provide tax advice. Please consult a qualified tax professional for such information. More information about UNest Advisers’ services is available in its ADV brochure and Customer Relationship Summary.

Testimonials, statements, and opinions presented on our website are applicable only to the individuals depicted. Results will vary and may not be representative of the experience of others. The testimonials are voluntarily provided, unpaid, and not given in exchange for products, services, or other benefits. Testimonials should not be considered a guarantee of future performance and do not reflect the experience of all clients.

© 2018-2025 UNest Holdings, Inc. All rights reserved.