5 UTMA Facts Every Parent Needs to Know in 2026

Most parents want to invest for their children, but between busy schedules, confusing financial jargon, and a growing list of account options, it's easy to never quite get started. If that sounds familiar, UTMA accounts might be exactly what you've been missing: flexible, powerful, and much simpler than you think.

Anyone Can Contribute, With No Limits

One of the most underappreciated features of a UTMA (Uniform Transfers to Minors Act) account is that it's open to everyone. Parents, grandparents, aunts, uncles, family friends. Anyone who wants to invest in a child's future can contribute. There are no restrictions on who can give.

And unlike many other savings vehicles, there are no annual contribution limits. You can contribute as much or as little as you'd like, whenever you'd like. This makes UTMA accounts an ideal vehicle for birthday gifts, holiday contributions, or even larger family transfers.

The First $1,350 Your Child Earns Is Tax-Free

Many parents assume that investment earnings in a child's account are taxed just like adult income. The reality is much friendlier, especially at lower earning levels.

Under the 2026 kiddie tax rules, the first $1,350 of unearned income (dividends, capital gains, interest) in your child's UTMA account is completely exempt from federal income tax. The next $1,350 is taxed at your child's rate, typically just 10%. Only amounts above $2,700 are taxed at the parent's marginal rate.

For most families in the early years of investing, their child's earnings will fall entirely in the tax-free or low-tax tiers.

You Can Give Up to $19,000 Per Year Gift-Tax-Free

Contributions to a UTMA account are considered gifts under IRS rules. In 2026, each person can give up to $19,000 per recipient per year without triggering any gift tax liability.

For married couples who elect to gift-split, that limit doubles to $38,000 per child per year, completely tax-free. Grandparents giving to multiple grandchildren can contribute significantly to each child's account annually without any tax implications.

Zero Restrictions on How the Money Is Used

This is where UTMAs truly stand apart. Unlike a 529 plan, which requires funds to be used for qualified educational expenses or face penalties, a UTMA account places no restrictions on how the money is ultimately spent.

College. A first car. A down payment on a home. Seed money for a business. Whatever your child's future holds, their UTMA account can support it without penalties, paperwork, or restrictions.

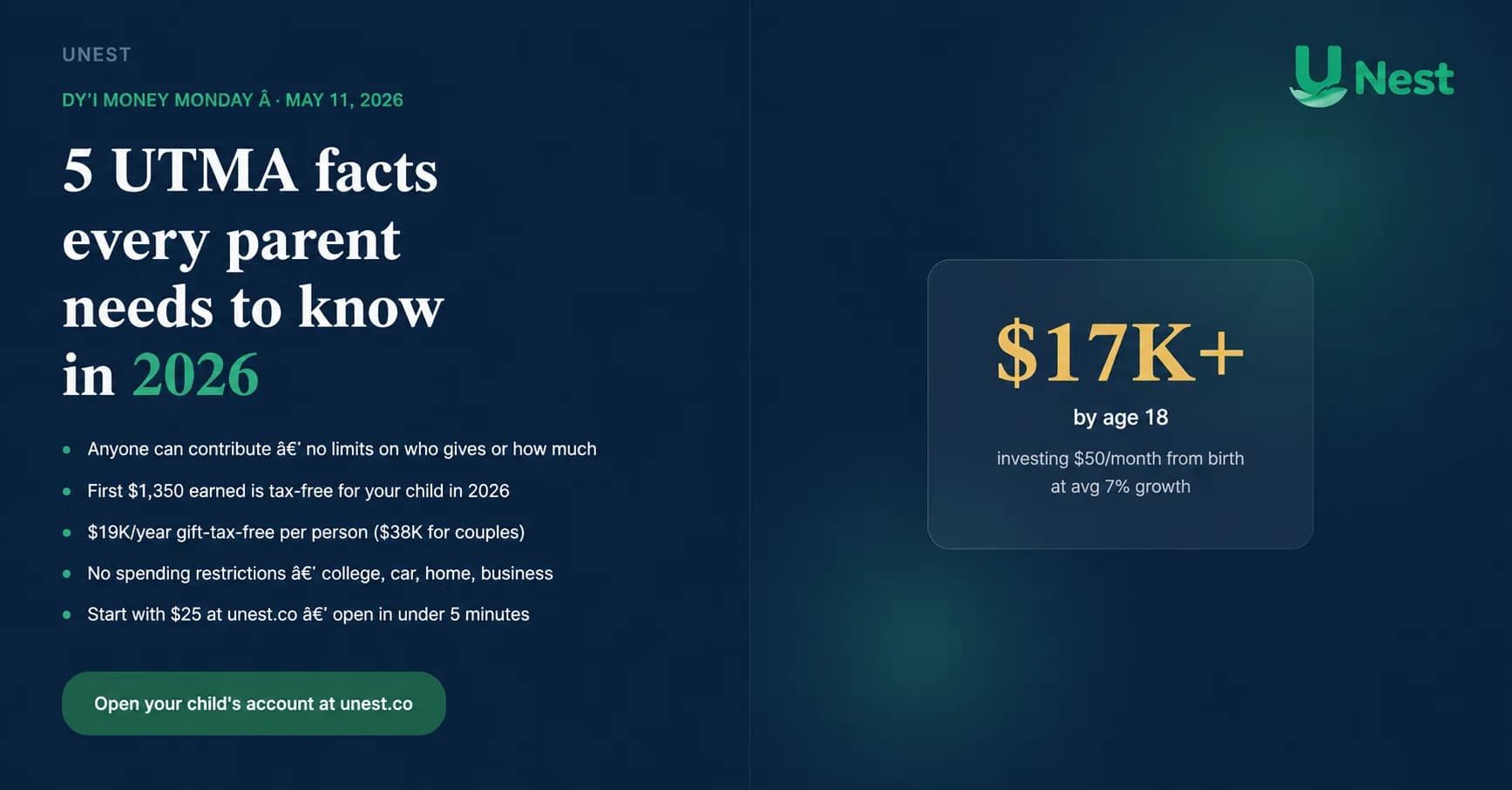

Starting Early Is the Whole Game

All the tax advantages and flexibility in the world matter less than one simple truth: time is the most powerful factor in investing. The earlier you start, the more compound growth does the heavy lifting for you.

Investing just $50 per month from birth at an average 7% annual growth rate grows to over $17,000 by age 18. Start at age 5 instead, and that drops to roughly $11,000. A $6,000 difference for the exact same monthly contribution.

Every month you wait is compound growth you can't get back. The best time to open your child's account was the day they were born. The second best time is today.

With UNest, you can open your child's UTMA account in under 5 minutes, starting with as little as $25. No financial advisor needed, no complicated paperwork.