UTMA vs. Savings Account: Which Wins for Your Child?

For most parents, opening a savings account for their child feels like the responsible move. And it is. But if your goal is to build meaningful, long-term wealth for your child over 18 years, a savings account alone may not be the most powerful tool available to you.

Here's an honest, side-by-side look at how a traditional savings account compares to a UTMA custodial investment account, and when each one makes the most sense.

The Core Difference

A savings account holds cash and earns interest at a fixed rate. A UTMA account invests in the market (stocks, ETFs, mutual funds) and earns returns based on market performance over time. That single difference compounds significantly over an 18-year horizon.

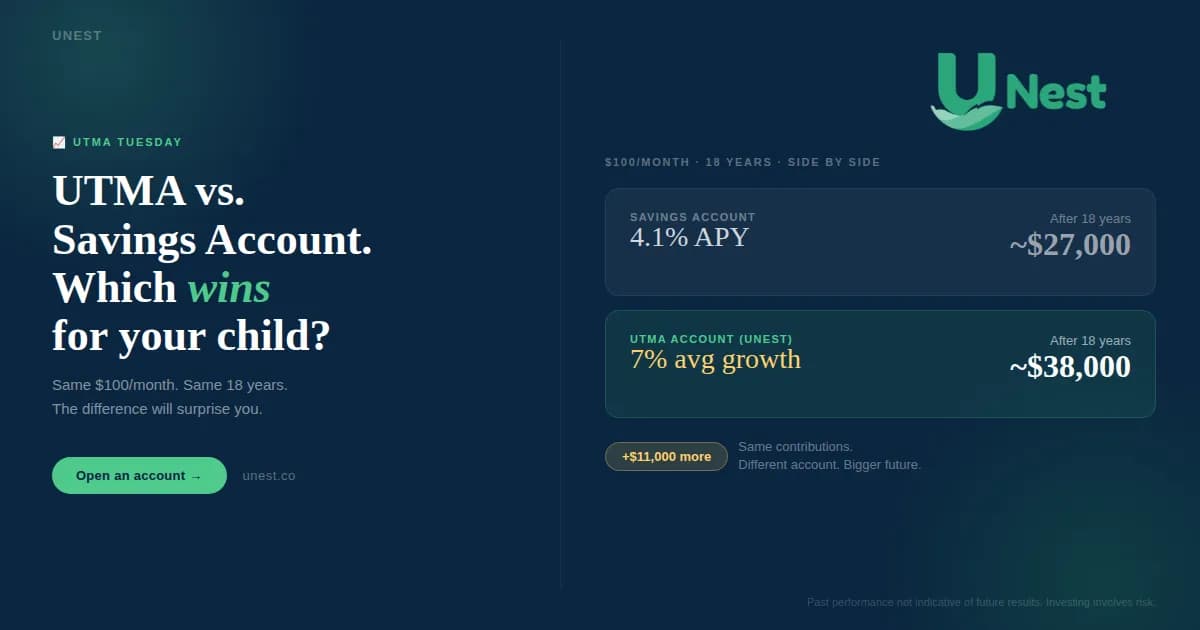

As of May 2026, the best available high-yield savings rate from FDIC-insured banks is around 4.1% APY. Meanwhile, UTMA accounts invested in diversified market assets have historically averaged 6 to 7% annual returns over long periods.

What the Numbers Actually Look Like

Put both accounts through the same test: $100 per month, from birth to age 18.

- Savings account (4.1% APY): approximately $37,000

- UTMA account (avg 7% growth): approximately $48,000

That's $11,000 more from the exact same monthly contribution over the same time period. The difference comes purely from how each account grows. That's the power of compounding at a higher rate over a long time horizon.

Market returns are not guaranteed. UTMA accounts involve investment risk and may lose value in the short term. The 6 to 7% figure represents long-term historical averages, not a promised return.

The UTMA's Hidden Advantages

Beyond growth potential, UTMA accounts offer structural advantages that savings accounts can't match.

Tax efficiency. The first $1,350 of your child's annual earnings in a UTMA account is completely federal income tax-free in 2026. The next $1,350 is taxed at your child's rate, typically just 10%. For most families in the early years, earnings will fall entirely in the tax-free tier.

No spending restrictions. Unlike a 529 plan, a UTMA has no restrictions on how the money is used. College, a car, a first home, a business. Whatever your child's life calls for.

Open contributions. Any adult can contribute. Parents, grandparents, aunts, uncles, family friends. Up to $19,000 per person per year is gift-tax-free in 2026 ($38,000 for married couples). Birthdays and holidays become investing opportunities.

When a Savings Account Is Still the Right Choice

Savings accounts aren't bad. They're the right tool for specific jobs:

- Emergency funds you may need to access quickly

- Short-term goals under 3 years

- Parents who want zero market risk

- Teaching basic saving habits to young children

When a UTMA Is the Better Move

- Long-term goals of 5 or more years

- College, a car, or a first home down payment

- Gifts from grandparents and extended family

- Building real, compounding generational wealth

- Introducing children to investing and the market

Use Both

You don't have to choose between them. Many financial experts recommend a two-account approach: a savings account for short-term stability and emergency access, and a UTMA for long-term investing and growth.

Think of the savings account as the foundation: stable, accessible, zero risk. The UTMA is the engine: market-driven, long-term, and built to outperform over an 18-year runway.

With UNest, you can open your child's UTMA account in under 5 minutes, starting at just $25. No financial advisor needed. No complicated paperwork. Just a smarter long-term strategy for your child's future.